Small Business Accounting 101: How to Set Up and Manage Your Books

If you’ve just launched or are about to launch your online store, congratulations! It takes uncommon passion and perseverance to get to where you are today.

However, as you know, small business owners often have a constant flood of satisfying milestones, coupled with expanding to-do lists. With your launch, you’ll need to get on top of the accounting tasks that come along with owning a store.

This list of accounting steps will give you the confidence to know you’ve covered your bases and are ready to move on to the next item on your small business finance to-do list.

Get your accounting in order ?

Bookkeeping 101

Bookkeeping is something that you either have to learn or outsource when you’re running a business. Luckily, it’s possible to learn how to manage your own books and there are a few notable benefits to tackling it yourself.

Accounting basics for small businesses

1. Open a bank account

After you’ve legally registered your business, you’ll need somewhere to stash your business income. Having a separate bank account keeps records distinct and will make life easier come tax time.

It also protects your personal assets in the unfortunate case of bankruptcy, lawsuits, or audits. And if you want funding down the line, from creditors or investors, strong business financial records can increase the likelihood of approvals.

Note that LLCs, partnerships, and corporations are legally required to have a separate bank account for business. Sole proprietors don’t legally need a separate account, but it’s definitely recommended.

Start by opening up a business checking account, followed by any savings accounts that will help you organize funds and plan for taxes. For instance, set up a savings account and squirrel away a percentage of each payment as your self-employed tax withholding. A good rule of thumb is to put 25% of your income aside, though more conservative estimates for high earners might be closer to one third.

Next, you’ll want to consider a business credit card to start building credit. Credit is important for securing funding in the future. Corporations and LLCs are required to use a separate credit card to avoid commingling personal and business assets.

Before you talk to a bank about opening an account, do your homework. Shop around for business accounts and compare fee structures. Most business checking accounts have higher fees than personal banking, so pay close attention to what you’ll owe.

To open a business bank account, you’ll need a business name, and you might have to be registered with your state or province. Check with the individual bank for which documents to bring to the appointment.

2. Track your expenses

The foundation of solid business bookkeeping is effective and accurate expense tracking. It’s a crucial step that lets you monitor the growth of your business, build financial statements, keep track of deductible expenses, prepare tax returns, and legitimize your filings.

From the start, establish an accounting system for organizing receipts and other important records. This process can be simple and old school (bring on the Filofax), or you can use a service like Shoeboxed. For US store owners, the IRS doesn’t require you to keep receipts for expenses under $75, but it’s a good habit nonetheless.

There are five types of receipts to pay special attention to:

- Meals and entertainment. Conducting a business meeting in a café or restaurant is a great option, just be sure to document it well. On the back of the receipt, record who attended and the purpose of the meal or outing.

- Out-of-town business travel. The IRS and CRA are wary of people claiming personal activities as business expenses. Thankfully, your receipts also provide a paper trail of your business activities while away.

- Vehicle-related expenses. Record where, when, and why you used the vehicle for business, and then apply the percentage of use to vehicle-related expenses.

- Receipts for gifts. For gifts like tickets to a concert, it matters whether the gift giver goes to the event with the recipient. If they do, then the expense would be categorized as entertainment rather than a gift. Note these details on the receipt.

- Home office receipts. Similar to vehicle expenses, you need to calculate what percentage of your home is used for business and then apply that percentage to home-related expenses.

Starting your business at home is a great way to keep overhead low, plus you’ll qualify for some unique tax breaks. You can deduct the portion of your home that’s used for business, as well as your home internet, cellphone, and transportation to and from work sites and for business errands.

Any expense that’s used partly for personal use and partly for business must reflect that mixed use. For instance, if you have one cellphone, you can deduct the percentage you use the device for business. Gas mileage costs are 100% deductible, just be sure to hold on to all records and keep a log of your business miles (where you’re going and the purpose of the trip).

3. Develop a bookkeeping system

Before we jump into establishing a bookkeeping system, it’s helpful to understand exactly what bookkeeping is and how it differs from accounting. Bookkeeping is the day-to-day accounting process of recording business transactions, categorizing them, and reconciling bank statements.

Accounting is a high-level process that looks at business progress and makes sense of the data compiled by the bookkeeper by building financial statements. As a new entrepreneur, you’ll need to determine how you want to manage your books:

- You can choose to go the DIY route and use software like QuickBooks or Wave. Alternatively, you could use a simple Excel spreadsheet.

- You have the option of using an outsourced or part-time bookkeeper that’s either local or cloud-based.

- When your business is big enough you can hire an in-house bookkeeper and/or accountant.

With so many options out there, you’re sure to find a bookkeeping solution that will suit your business needs.

Canadian and US business owners need to determine whether they’ll use the cash or accrual accounting methods. Let’s take a look at the difference between the two.

- Cash method. Revenues and expenses are recognized at the time they are actually received or paid.

- Accrual method. Revenues and expenses are recognized when the transaction occurs (even if the cash isn’t in or out of the bank yet) and requires tracking receivables and payables.

Technically, Canadians are required to use the accrual method. To simplify things, you can use the cash method throughout the year and then make a single adjusting entry at year end to account for outstanding receivables and payables for tax purposes.

US business owners can use cash-based accounting if revenues are less than $5 million, otherwise they must use the accrual method.

Bookkeeping 101

Bookkeeping is something that you either have to learn or outsource when you’re running a business. Luckily, it’s possible to learn how to manage your own books and there are a few notable benefits to tackling it yourself.

4. Set up a payroll system

Many online stores start out as a one-person show. When you’ve reached the point where it makes sense to hire outside help, you need to establish whether that individual is an employee or an independent contractor.

For employees, you’ll have to set up a payroll schedule and ensure you’re withholding the correct taxes. There are lots of services that can help with this, and many accounting software options offer payroll as a feature.

For independent contractors, be sure to track how much you’re paying each person. American business owners may be required to file 1099s for each contractor at year end (you’ll also need to keep their name and address on file for this).

5. Investigate import tax

Depending on your business model, you may be planning to purchase and import goods from other countries to sell in your store. When importing products, you’ll likely be subject to taxes and duties, which is worth noting if you run a dropshipping business. These are the fees your country imposes on incoming goods. Learn about importing goods into the US and Canada, and the associated taxes, so you know the rules from the get-go.

Also, if you’re importing goods, a duty calculator can help you estimate the fees in your own business and plan for costs.

6. Determine how you’ll get paid

When sales start rolling in, you’ll need a way to accept payments. If you’re a North American store owner on Shopify, you can use Shopify Payments to accept debit or credit card orders. This saves you the hassle of setting up a merchant account or third-party payment gateway.

If you want to accept credit card payments without using Shopify Payments, you’ll need a merchant account or you can use a third-party payment processor, like PayPal, Stripe, or Square. A merchant account is a type of bank account that allows your business to accept credit card payments from customers.

If you use a third-party payment processor, fees vary. Some processors charge an interchange plus rate, typically around 2.9% + $0.30 per transaction. Others charge flat fees for each transaction, while some have a monthly membership model for unlimited transactions. You can consult this list to help you find a payment gateway that will work for your location.

Free: Business Plan Template

Business planning is often used to secure funding, but plenty of business owners find writing a plan valuable, even if they never work with an investor. That’s why we put together a free business plan template to help you get started.

Get the business plan template delivered right to your inbox.

Almost there: please enter your email below to gain instant access.

We’ll also send you updates on new educational guides and success stories from the Shopify newsletter. We hate SPAM and promise to keep your email address safe.

7. Establish sales tax procedures

The world of ecommerce has made it easier than ever to sell to customers outside of your state and even country. While this is a great opportunity for brands with growth goals, it introduces confusing sales tax regulations.

When a customer walks into a brick-and-mortar retail store, they pay the sales tax of whatever state or province they make the purchase in, no matter if they live in that city or they’re visiting from somewhere around the world. However, when you sell online, customers may be located in different cities, states, provinces, and even countries.

Canadian store owners only need to start collecting GST/HST when they have revenues of $30,000 or more in a 12-month period. You can submit the GST/HST you collect in installments. If you want, you can collect GST/HST even if you don’t earn this much in revenue, and put it toward input tax credits.

Selling to international customers can be easier than domestic sales. Canadian store owners don’t need to charge GST/HST to customers who are outside of Canada.

For US store owners, sales tax gets a bit trickier. You’ll need to determine if you operate your business in an origin-based state or a destination-based state. In the former, you must charge sales tax based on the state where you run your business. The latter requires sales tax to be applied based on the purchaser’s location.

International purchases are tax exempt for US-based businesses. This can all get a bit complicated, so check in with your accountant for detailed information about your specific state’s regulations regarding international sales tax.

8. Determine your tax obligations

Tax obligations vary depending on the legal structure of the business. If you’re self-employed (sole proprietorship, LLC, partnership), you’ll claim business income on your personal tax return. Corporations, on the other hand, are separate tax entities and are taxed independently from owners. Your income from the corporation is taxed as an employee.

Self-employed people need to withhold taxes from their income and remit them to the government in lieu of the withholding that an employer would normally conduct. For American store owners, you’ll need to pay estimated quarterly taxes if you’ll owe more than $1,000 in taxes this year. Canadians have it a little easier; if your net tax owing is more than $3,000, you’ll be required to pay your income tax in installments.

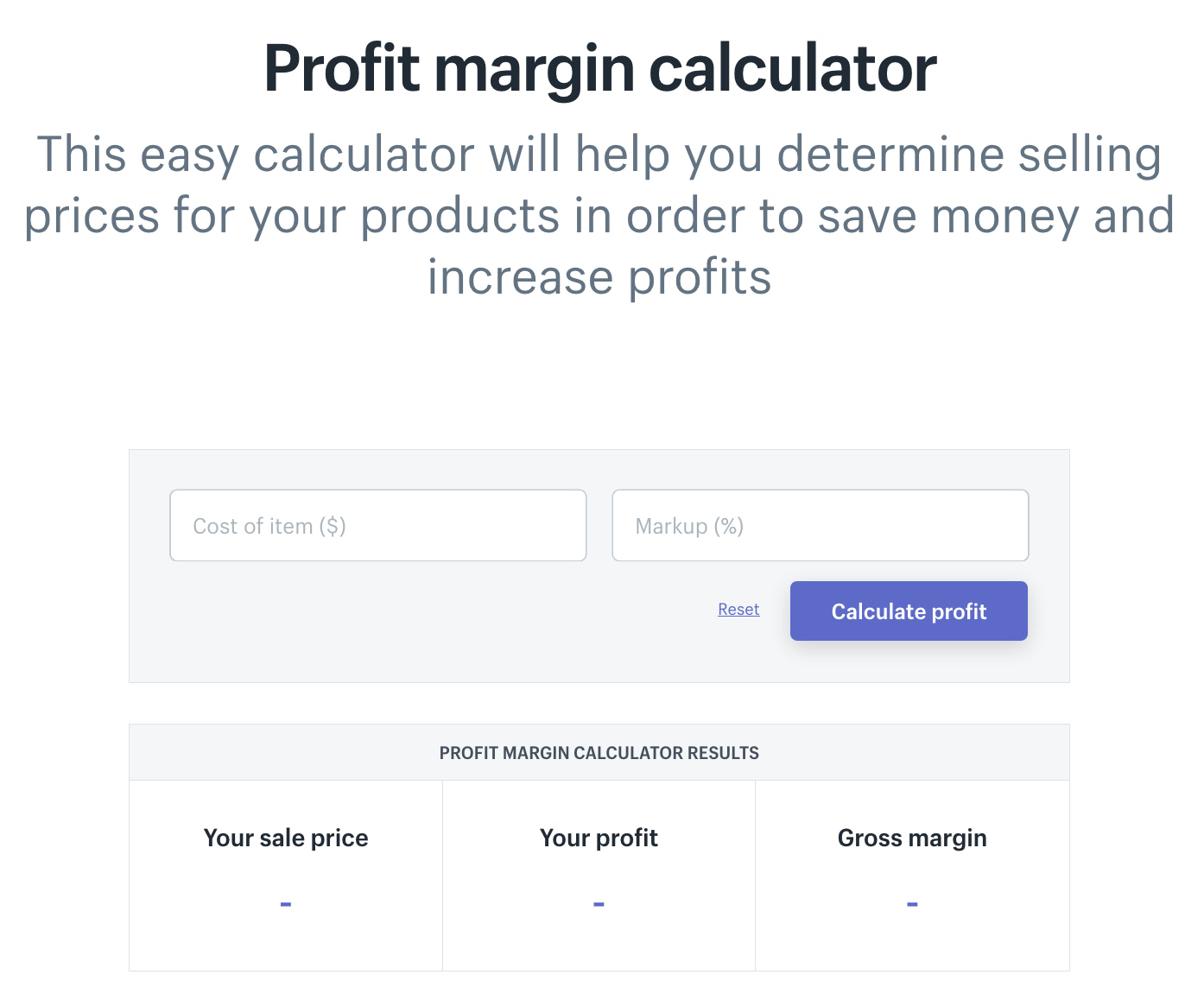

9. Calculate gross margin

Improving your store’s gross margin is the first step toward earning more income overall. In order to calculate gross margin, you need to know the costs incurred to produce your product. To understand this better, let’s quickly define both cost of goods sold (COGS) and gross margin.

- COGS. These are the direct costs incurred in producing products sold by a company. This includes both materials and direct labor costs.

- Gross margin. This number represents the total sales revenue that’s kept after the business incurs all direct costs to produce the product or service.

Here’s how you can go about calculating gross margin:

Gross margin (%) = (revenue – COGS) / revenue

You can also use our free profit margin calculator to plug in your numbers for a quick calculation.

The difference between how much you sell a product for and how much the business actually takes home at the end of the day is what truly determines your ability to keep the doors open.

10. Apply for funding

There are many scenarios where a growing ecommerce business might need to secure external business financing, be it through a line of credit, investors, a small business loan, or even a business partner.

For instance, you might have an unexpected downturn in sales due to uncontrollable external circumstances, or maybe you need a financial boost during slow periods in a seasonal business. Brands with big growth goals often need to secure funding to make investments in new product developments, inventory, retail stores, hiring, and more.

Remember, to get a small business loan, you’ll likely have to provide financial statements—a balance sheet and income statement at the very least, possibly a cash flow statement as well.

But before you sign off on the debt, it’s important to make sure the numbers make sense. In other words, it’s a good idea to calculate the ROI of the loan. Add up all the expenses you need the loan to cover, the expected new revenue you’ll get from the loan, and the total cost of interest. You can use our business loan calculator to find out the total cost.

11. Find high-quality accounting partners

As a business owner, you’ll want to have an understanding of generally accepted accounting principles (GAAP). It’s not a rule, but it helps you measure and understand your company’s finances.

If you need a little extra financial planning help or guidance, many small business accountants and financial professionals can help you get more control of your money. There are a few individuals you might want to consider enlisting:

- Accountant. A small business accountant can advise at many different points, including your business structure, creating financial statements, obtaining necessary licenses and permits, and even writing a business plan.

- Certified public accountant (CPA). In case of an audit, a CPA is the only individual who can legally prepare an audited financial statement.

- Bookkeeper. The bookkeeper manages the day-to-day records, regularly reconciling accounts, categorizing expenses, and managing accounts receivable/accounts payable.

- Tax preparer. Your tax preparer fills out necessary forms and may file them on your behalf during tax season. Some will also set up your estimated tax payments.

- Tax planner. These professionals help optimize your taxes before you file them, helping you learn ways to lower your tax burden.

12. Periodically reevaluate your methods

When you first start out you may opt to use a simple spreadsheet to manage your books, but as you grow you’ll want to consider more advanced methods like QuickBooks or Bench. As you keep growing, continually reassess the amount of time you’re spending on your books and how much that time is costing your business.

The right bookkeeping solution means you can invest more time in the business with bookkeeping no longer on your plate and potentially save the business money. Win-win!

Best small business accounting software

Every business owner needs good accounting software to remove manual data entry and save time. Accounting software is something you use to access financial information quickly and easily. It lets you check bank balances, understand revenue and costs, predict profitability, predict tax liabilities, and more.

Once you connect your business bank accounts and credit cards to a software, transactions show up in a queue and are grouped into categories. You can find all this information on your chart of accounts. Once you approve of the categories, transactions automatically settle in your financial statements.

Some features to look for in your account software include:

- Platform integrations. You want your accounting software to easily integrate with your ecommerce platform, as well as third-party tools like contract management and more.

- Broad reporting. Most accounting software provides basic reporting. You’ll want one that provides advanced reports, such inventory and expenses, so you can monitor financial health quickly.

- Sales tax configuration. Knowing what sales tax you’re required to pay and how much to collect is confusing. Find an accounting software that makes it easy to account for sales tax.

- Excellent support. Check reviews and support ratings to see how a software company’s customer support is. Aim for 24/7 support and self-service centers.

There are many user-friendly accounting software options for small businesses, ranging from free to paid models. You can also browse the Shopify App store for an accounting software that will seamlessly integrate with your ecommerce store.

Check out the following accounting software you could use to manage your books.

Xero

Xero is a cloud-based accounting system designed for small and growing businesses. You can connect with a trusted adviser and gain visibility into your financial health. It can be accessed from any device. Plus, with Xero’s advanced accounting features, you can view cash flows, transactions, and other financial information from anywhere.

Benefits:

- Inventory and stock management

- Affordable pricing

- Connects to major banks

- Easy to view and customizable reports

- Contact database and segmentation

- Payroll

- Mobile app

- Bank reconciliation

QuickBooks Online

QuickBooks Online is a small business accounting software run by Intuit. You can use it to snap and store receipts for expenses, track your income and expenses, and more.

QuickBooks shows all your costs, such as inventory and maintenance costs, and every sale your business makes over a period of time. It also offers inventory automation using perpetual inventory tracking, so your sales and inventory cost are updated every time you make a sale. You can also integrate QuickBooks with Shopify to stay organized and up to date.

Benefits:

- Mobile app

- Cloud-based

- Mileage tracking

- Contractor management

- Inventory tracking

- Separating business and personal expenses

Wave

Wave is a web-based accounting solution built for small businesses. With its bank reconciliation feature, you can link your bank accounts, PayPal accounts, and other data sources to see real-time business transactions. You can also generate reports such as accounts receivable, balance sheets, sales tax reports, and accounts payable.

Benefits:

- Affordable

- Competitive credit card processing fees

- Free accounting and receipt scanning

- No transaction or billing limits

- Unlimited number of users

- Mobile app

FreshBooks

FreshBooks is a cloud-based accounting and invoice management software for small businesses. It offers expense management, core accounting, and everything you need to take care of basic bookkeeping.

Benefits:

- Easy to use

- Integrates with Shopify

- Simple pricing

- Customizable invoices

- Detailed self-service support

Know your numbers to grow your business

Starting a business can be an overwhelming process, but if you follow this list, you’ll have your new store’s finances in order from the beginning. From opening the right type of bank account to determining how much you’ll bring in per product, these tasks will all contribute to your business’ success, now and as it grows.

Ready to create your first business? Start your free 14-day trial of Shopify—no credit card required.

Small business accounting FAQ

How do I do accounting for my small business?

How much should I pay an accountant for my small business?

What does an accountant do for a small business?

- Form your business

- Help write a business plan

- Audit your cash flow

- Find cost-cutting opportunities

- Advise on business strategy

- Manage debt

- Chase down payments

- Write and submit loan applications

- Plan budgets

- Set up your accounting software

- Manage inventory

- Recommend business tools

- Help open new bank accounts

- Oversee payroll

- Year-end financial reporting

- Prevent audits

- Advise on personal finances

What does a bookkeeper do for a small business?

- Reconcile accounts

- Record transactions

- Manage accounts receivable and accounts payable

- Adjust entries

- Prepare financial statements

- Send invoices

- Set up and manage technology and tools

- Stay up to date on laws and regulations

- Basic payroll

- Work with your accountant, tax preparer, and tax planner